Key Points:

- Seven & i Holdings, the parent company of 7-Eleven, has rejected a $14.86 per share takeover bid from Canadian convenience store giant Alimentation Couche-Tard.

- The proposal was criticized as “opportunistically timed” and “grossly undervaluing” the company’s growth potential.

- Significant regulatory challenges from U.S. antitrust agencies are also a major concern.

Tokyo, Japan – Seven & i Holdings, the powerhouse behind the global 7-Eleven convenience store empire, has firmly rejected a $14.86 per share takeover bid from Canadian convenience store giant Alimentation Couche-Tard. The Tokyo-based conglomerate, which operates more than 85,000 stores worldwide, deemed the offer as “grossly undervaluing” its intrinsic value and future growth prospects.

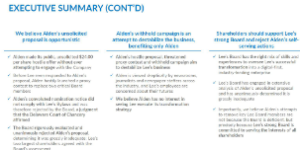

In a decisive statement filed with the Tokyo Stock Exchange, Stephen Dacus, chairman of the special committee tasked with evaluating the proposal, slammed the bid as “opportunistically timed.” He argued that the offer fails to recognize the substantial avenues Seven & i has to unlock shareholder value in the near to medium term.

Regulatory Hurdles Pose Significant Risks

Beyond the perceived undervaluation, Seven & i cited major regulatory challenges as a key reason for rejecting the offer. The proposal was criticized for not adequately addressing the significant hurdles it would face from U.S. antitrust agencies. “The proposal does not consider the multiple and significant challenges the takeover would face from U.S. anticompetition agencies,” Dacus wrote in a letter addressed to Couche-Tard’s Chair, Alain Bouchard.

Dacus also pointed out that the proposal lacked a clear strategy for navigating these regulatory obstacles, which could potentially delay or derail the transaction altogether. “You have provided no indication at all of your views as to the level of divestitures that would be required or how they would be effected,” he added.

Shareholder Frustration and Calls for Reform

The rejection of the offer has sparked mixed reactions among shareholders. Ben Herrick, associate portfolio manager at U.S. investment firm Artisan Partners, criticized Seven & i’s management for not doing enough to enhance corporate value. Speaking on CNBC’s “Squawk Box Asia,” Herrick argued that the offer “highlights the fact that this management team and the board have not done all of the things in their power to increase the corporate value of this organization.”

Artisan Partners, which holds a stake of just over 1% in Seven & i, has urged the company to consider the bid and accelerate its restructuring efforts. Herrick believes that the company’s international operations, particularly outside the U.S., present a “huge opportunity” for growth that has been largely overlooked.

He also expressed frustration over the slow pace of reforms, noting that Seven & i President Ryuichi Isaka’s “100-day plan” to revamp the company’s general merchandise store Ito-Yokado, announced in 2016, has yet to yield significant results. “We’re approaching day 3,000 here,” Herrick said, emphasizing the need for a faster, more aggressive approach to reform.

A Divided Outlook on the Future

Despite the criticism, some stakeholders believe that Seven & i is on the right track. Richard Kaye, portfolio manager at Comgest, argued that the company is already excelling in areas like logistics and product innovation. He questioned whether a foreign acquirer like Couche-Tard could significantly improve on the company’s current performance. “The company is doing a phenomenal job,” Kaye said, adding that there’s no pressing need for a radical overhaul.

Conclusion

As Seven & i navigates the complexities of the global market, the rejection of Couche-Tard’s bid underscores the company’s commitment to maintaining control over its destiny. With a focus on unlocking shareholder value and addressing regulatory concerns, the company’s future remains a focal point in the competitive convenience store industry.

The article discusses the rejection of a takeover bid by Seven & i Holdings, the parent company of 7-Eleven, from Alimentation Couche-Tard, a Canadian convenience store operator. Here’s additional data and context to expand on the article:

1. Background on Seven & i Holdings

- Company Overview: Seven & i Holdings is a major Japanese retail group, best known as the parent company of 7-Eleven, one of the world’s largest convenience store chains. The company also operates other businesses, including supermarkets, department stores, and financial services.

- Global Presence: 7-Eleven operates over 85,000 stores globally, with significant footprints in Japan, the United States, and Southeast Asia. It’s a leading brand in the convenience store sector, known for its extensive network and innovative retail strategies.

2. Alimentation Couche-Tard’s Business Profile

- Company Overview: Alimentation Couche-Tard is a Canadian multinational operator of convenience stores. It operates under several brand names, including Circle K, and has a strong presence in North America, Europe, and other regions.

- Growth Strategy: Couche-Tard has been aggressively expanding through acquisitions, aiming to strengthen its global footprint in the convenience store market. The proposed acquisition of Seven & i would have been the largest-ever foreign takeover of a Japanese company.

3. Takeover Proposal Details

- Offer Valuation: Couche-Tard’s offer to acquire Seven & i was priced at $14.86 per share, which was seen as undervaluing the company by Seven & i’s special committee. The total valuation of the offer was significant, considering Seven & i’s vast global operations.

- Strategic Intent: Couche-Tard’s interest in Seven & i likely stems from the potential synergies in global operations, particularly in the convenience store sector. By acquiring Seven & i, Couche-Tard could potentially consolidate its market position and achieve economies of scale.

4. Regulatory Concerns

- Antitrust Issues: The acquisition faced potential hurdles from U.S. antitrust regulators, given the size and market power of the combined entity in the convenience store market. The concerns revolved around the potential for reduced competition, particularly in the U.S. market where both companies have significant operations.

- Divestiture Requirements: To gain regulatory approval, Couche-Tard might have needed to divest certain assets or operations, a process that could be complex and time-consuming. Seven & i’s rejection highlighted the lack of clarity on how these regulatory challenges would be managed.

5. Shareholder Dynamics

- Artisan Partners’ Position: Artisan Partners, a minority shareholder in Seven & i, expressed dissatisfaction with the management’s efforts to unlock value. They believed that the offer from Couche-Tard could have been a catalyst for necessary reforms within the company.

- Diverging Opinions: While some shareholders were frustrated with the pace of change at Seven & i, others believed the company was on the right track with its current strategy. This division reflects broader debates about the company’s future direction.

6. Seven & i’s Restructuring Plans

- Recent Changes: In April, Seven & i announced a restructuring plan aimed at optimizing its global operations and divesting underperforming assets. This plan is seen as crucial to enhancing the company’s focus on its core convenience store business.

- Long-Term Vision: The company is aiming to expand its 7-Eleven brand globally, particularly in regions where convenience store penetration is still growing. This focus is expected to drive future growth and increase shareholder value.

7. Market Impact and Investor Reactions

- Stock Performance: The announcement of the rejection, along with the market’s response to the takeover bid, could influence Seven & i’s stock performance in the short term. Investors may react to both the perceived undervaluation by Couche-Tard and the company’s future growth prospects.

- Industry Implications: The rejection of such a significant takeover bid highlights the challenges in cross-border M&A, especially in highly regulated industries like retail. It also underscores the importance of strategic fit and regulatory considerations in large-scale acquisitions.